FTAI Aviation CEO and chairman Joe Adams called out a report from Muddy Waters Research, calling it “baseless and nonsensical” in a stock filing on January 21, 2025.

The report in question, published January 15, 2025, claimed FTAI was “short” because its “financial reporting is highly misleading”.

“We believe revenue from true maintenance and individual off-the-rack module sales are materially lower than reported,” the Muddy Waters Research report stated. “FTAI, in our view, is misleading investors by reporting one-time engine sales as maintenance repair & overhaul (MRO) revenue in its aerospace products (AP) segment. It appears that FTAI's AP revenue growth is due to trading whole engines (i.e. asset sales).”

The report estimated that around 80% of the company's AP adjusted EBITDA is gains on sale, which the report said it believes to be “largely from selling whole engines”.

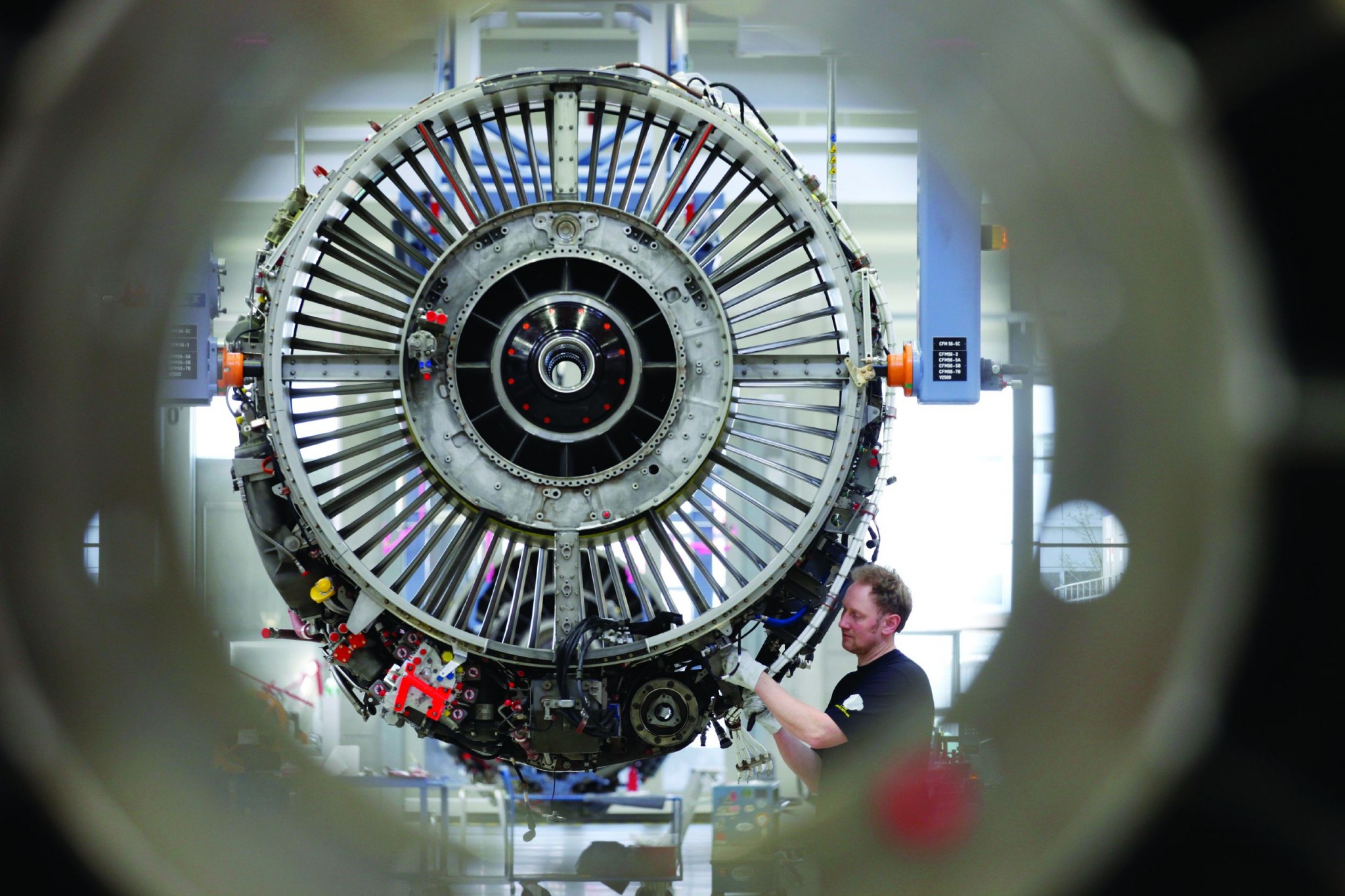

FTAI Aviation provides aftermarket power and maintenance services for commercial jet engines. The company owns and maintains commercial jet engines, focussing on the CFM56 and V2500 engines.

The report continued: “The goal of these misrepresentations appears to be to generate a valuation materially greater than that of a leasing business. Fortress sold significant stock in a May 2024 secondary offering on the back of FTAI's misleading narrative."

“We strongly disagree with the assertions made in the report,” said Adams. He said the report “mischaracterises” FTAI, stating the claims were “misrepresentations”.

He said the company's depreciation policy and methodology has remained the same since its initial public offering (IPO) in 2015.

“Current residual values are approximately 50% of the acquisition cost and are depreciated over the expected time between shop visits (two to six years)," continued Adams. He further pointed to the company's return on gross assets, which he said stands at around 10% for the first nine months of 2024, which is “in line with or exceeds that of industry peers”.

The report included comments from former FTAI executives, with one claiming that FTAI would count a whole engine sale as module sales, so that the “module factory numbers are much higher than what real customer demand for the factory is”, the unnamed executive said in report.

While the executive is no longer at the company, they said this approach to reporting was the “line of thought” while at the company. Another former FTAI executive quoted in the report said: “They sell between 60 and 80 engines a year and they report 95% into the aerospace business… They do 80 whole engine sales a year that they count as modules."

Furthermore, Muddy Waters Research spoke with an unnamed industry export, noting that very few companies are purchasing standalone modules. “I just don't believe that there's 82 standalone modules being sold," the expert said in the report. The expert said it would be more believable if these sold modules comprised of 20 standalone modules and the rest being whole engines counted as module sales.

During the company's third quarter 2024 earnings call, Adams had stated the company had stopped providing detail on module sales.

The company expects an adjusted EBITDA of around $1.1 to $1.15bn in 2025. This includes approximately $500 million from its aviation leasing segment and around $600 to $650 million from its AP segment.

Furthermore, Adams noted its strategic capital initiative launched in December 2024 with third party institutional investors. The first partnership is focused on acquiring on-lease 737NG and A320ceo aircraft.

“We believe this market opportunity will allow for the deployment of $3bn+ of capital annually,” said Adams. “This first partnership is also in the process of acquiring 46 on-lease narrowbody aircraft from FTAI for an estimated net purchase price of $549 million.”

In addition, the company has received two out of the five parts manufacturer approval (PMA), with the certification for the next part being “very close”. Adams said this next certification will drive production at its facilities and help grow the company's margins.